Social Security Break Even – How to Calculate Your Break Even Age

Social security benefits offer you a choice: You can start collecting retirement benefits as early as age 62; but if you wait till you’re older, you’ll be entitled to larger benefit checks.

It’s impossible to know which option will pay off better in the long run — among other things, that would entail knowing exactly when you are going to die. Still, understanding the trade-off between when you start collecting social security benefits and the size of those checks will help you make a more informed decision.

When Can I Collect Social Security?

Eligibility for your full social security benefit amount is based on what the Social Security Administration considers your full retirement age. If you were born before 1938, your full retirement age was 65. If you were born in 1960 or later, your full retirement age is 67. If you were born from the period of 1938 through 1959, your full retirement age is somewhere between 65 and 67.

The Social Security Administration offers a retirement age calculator that allows you to enter the year of your birth and find your full retirement age.

If you are willing to settle for less than your full benefit, you can start collecting social security as early as age 62. However, the sooner you start collecting social security, the smaller your benefit will be — and it will remain smaller than your full benefit amount for the rest of your life.

Conversely, if you delay collecting social security past full retirement age, you can actually earn more than your full benefit once you finally start collecting. Your benefit will increase each year you delay past your full retirement age up until age 70. Once you are past 70, waiting will no longer increase your benefit so there is no reason to delay collecting social security any longer than age 70.

Find Banks Savings Accounts with the Best Rates

Finding the bank with the highest savings account interest rate is as simple as using our search tool. Try it now and find your high-interest savings account.

What Is Breakeven Age for Collecting Social Security?

So there is a trade-off between when you start collecting social security and the size of your benefit; but what does this trade-off look like? The following table is based on an example provided by the Social Security Administration. It assumes a person would be entitled to a $1,300 benefit upon reaching full retirement age at 66 years and 4 months.

As you can see, each year you delay collecting raises the benefit. The amount of those increases varies, but on average the dollar amount increases by 7.4% each year. However, it would be inaccurate to liken delaying to earning a 7.4% return on your money because that doesn’t take into account that the earlier you start collecting, the more years’ worth of benefits you get.

In fact, this is the heart of the dilemma: you will come out ahead at first by starting to collect benefits earlier, because you will receive those benefits for more years. However, if you live long enough, eventually the larger benefits you would be entitled to if you waited longer would catch up with the amounts you would have earned by collecting earlier.

Here’s an example: Using the above figures, suppose you could start collecting a $953 monthly benefit at age 62. By the time you reach age 70, you will already have collected a cumulative total of $91,488 in benefits.

However, at that point, had you waited you would have been entitled to $1,681 monthly benefit — $728 a month more, or $8,736 more for a full year. In time, these larger benefits would make the cumulative total received larger than you would have accumulated by starting earlier. In this example, that point would be reached at around age 80 1/2.

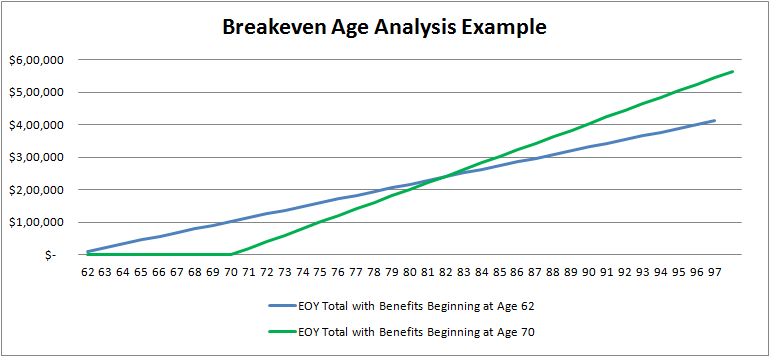

This is known as the breakeven age – the point at which you would earn more by delaying collecting social security than you would by collecting a smaller benefit earlier. In other words, in social security terms, a breakeven age is the age you’ll be when the cumulative payouts for two benefit start dates equal each other.

How to calculate your Breakeven Age

One way to understand breakeven age is by thinking of your benefit choices as two different potential streams of income. In the example given above, you would have a choice of earning $953 a month beginning at age 62 or $1,681 a month beginning at age 70.

Multiply those monthly amounts by 12 to get their yearly value, and then project the cumulative amounts earned each year into the future. The smaller stream of income would have a head start because it would begin at age 62, while the larger stream wouldn’t start till age 70 but would start catching up from that point on. If you look at the cumulative total for each stream of income from then on, you can see when the breakeven point is reached.

Since different people are entitled to different social security benefits, your breakeven age will depend on the amount of your benefits. You can get an estimate of what social security benefits you are entitled to by using the Social Security Administration’s Retirement Estimator.

Be advised that this tool only provides an estimate of your benefit. (The actual amounts could change based on your future earnings history, changes in the law, and inflation.) But this estimate provides you with a sense of what benefit amounts you may be entitled to at different ages, and you can use those amounts as the basis for your breakeven calculation.

This type of calculation is not just something you should think about doing as you near retirement age, because it is also a cornerstone to long-term retirement planning. Until you get a feel for what you can expect from social security and when you will start to receive it, you can’t reliably plan on how much retirement income you’ll need to accumulate in savings vehicles such as 401(k) plans, IRAs or Health Savings Accounts.

Factor in Mortality and Marriage

Of course, the trick to coming out ahead by starting to collect social security later is to live long enough to reach the breakeven age.

Whether or not you will be able to do that, though, is impossible to know. The Social Security Administration does provide a life expectancy calculator that can provide some general guidance. For example, according to this calculator, a 62-year-old male can expect to live to age 83.6. In the example given earlier, the breakeven age for coming out ahead by delaying collecting social security was 80, so on average it would make sense for a person in that situation to delay collecting social security to earn the maximum benefit.

However, the life expectancy calculator is based on average life spans. Your health and family history are also important considerations in estimating how your life span is likely to relate to the average.

It also makes a difference if you are married. Survivor benefits for spouses are increased if you delay when you start to collect social security. So, if you are married, there is a better chance that at least one of you will live long enough to reach the breakeven age. According to the Social Security Administration, a married couple at age 65 today has a 50-50 chance of at least one spouse living till age 90.

In the example shown previously, the monthly benefit available at age 70 was 76 percent larger than the one available at age 62. Since survivor benefits are based on a percentage of the deceased’s benefit, delaying collecting social security could increase a survivor’s benefit by a similar proportion.

How to Decide at What Age to Collect Social Security

Calculating your breakeven age is helpful, but it is far from the last word on determining the right age to collect social security. Once you know the breakeven age for two benefit scenarios, you have to consider your chances of reaching that age in the context of a number of factors including health, family history and marital status.

You also have to consider the potential lifestyle benefits of collecting social security sooner, including whether you have a pressing need for that money. Finally, if you delay collecting social security, think about where you will come up with money to live on in the meantime and what you might be giving up by not investing that money.